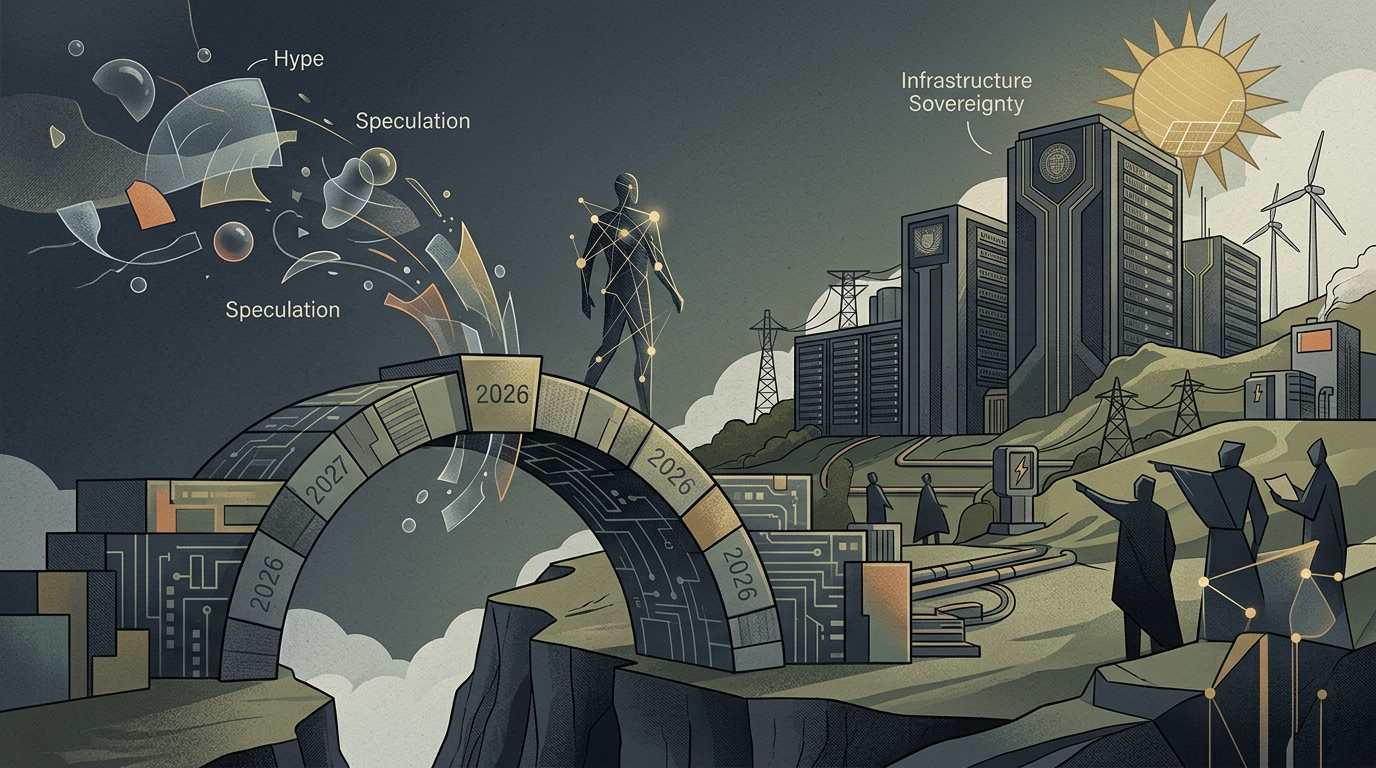

The 13% Correction: A Necessary Filter

As we close out June 2026, the global markets are grappling with a significant 13% correction in AI-related equities. For the uninitiated, this might look like the bursting of a bubble; however, for the seasoned market observer, it represents a 'stress test' for real enterprise value. We are witnessing the 'Great AI Divergence,' where retail-driven hype is being replaced by strategic capital. The market is no longer rewarding promises; it is rewarding integration and infrastructure.

The data suggests that this is not a retreat from technology, but a relocation of capital. While speculative software valuations have taken a hit, the 'Memory Chip Renaissance' is in full swing. The demand for HBM (High Bandwidth Memory) and next-generation storage has driven unprecedented profit margins for hardware giants. Companies like Dell have successfully pivoted from legacy PC manufacturers to 'AI Sovereigns,' providing the necessary hardware backbone for the 72% of enterprises that are now actively deploying AI solutions in their daily operations.

The Infrastructure Bottleneck: The New 'Data Center Wall'

The primary threat to AI ROI (Return on Investment) in the second half of 2026 is no longer algorithmic capability, but physical infrastructure. The 'Data Center Wall'—a combination of energy scarcity, cooling limitations, and real estate bottlenecks—has become the most critical variable in corporate valuations. Investors are now looking at energy-efficient hardware and proprietary power solutions as the primary indicators of a company's long-term viability in the AI space.

The $20 billion gambit for 'Silicon Sovereignty' is not just about chips; it is about the entire stack of physical assets required to sustain digital intelligence.

This shift toward 'Silicon Sovereignty' is prompting massive capital expenditures. We are seeing a move toward vertically integrated models where tech giants are investing directly in energy grids and specialized semiconductor fabs. This is a capital-intensive phase that favors large-cap players with deep pockets, potentially squeezing out smaller startups that cannot secure the necessary compute resources.

Greek Market Implications: Digital Resets and Enterprise Agility

In the Greek landscape, the impact of these global trends is manifesting in unique ways. The recent legislative and digital 'reset' for 2 million Greek debtors, powered by AI-driven administrative tools, serves as a prime example of how digital transformation is moving from the private sector into the core of the national economy. This automation of debt management is expected to improve bank balance sheets and increase liquidity in the local market.

For Greek SMEs, the message is clear: the correction in tech stocks offers a strategic window to invest in productivity-enhancing tools at more reasonable valuations. As the 'Golden Handcuffs' of high-salary tech roles begin to loosen—evidenced by the trend of veterans moving into tangible, non-digital industries—the talent pool for local digital transformation is becoming more accessible. The Greek business ecosystem must leverage this period of market stabilization to integrate AI not as a buzzword, but as a fundamental tool for operational efficiency.