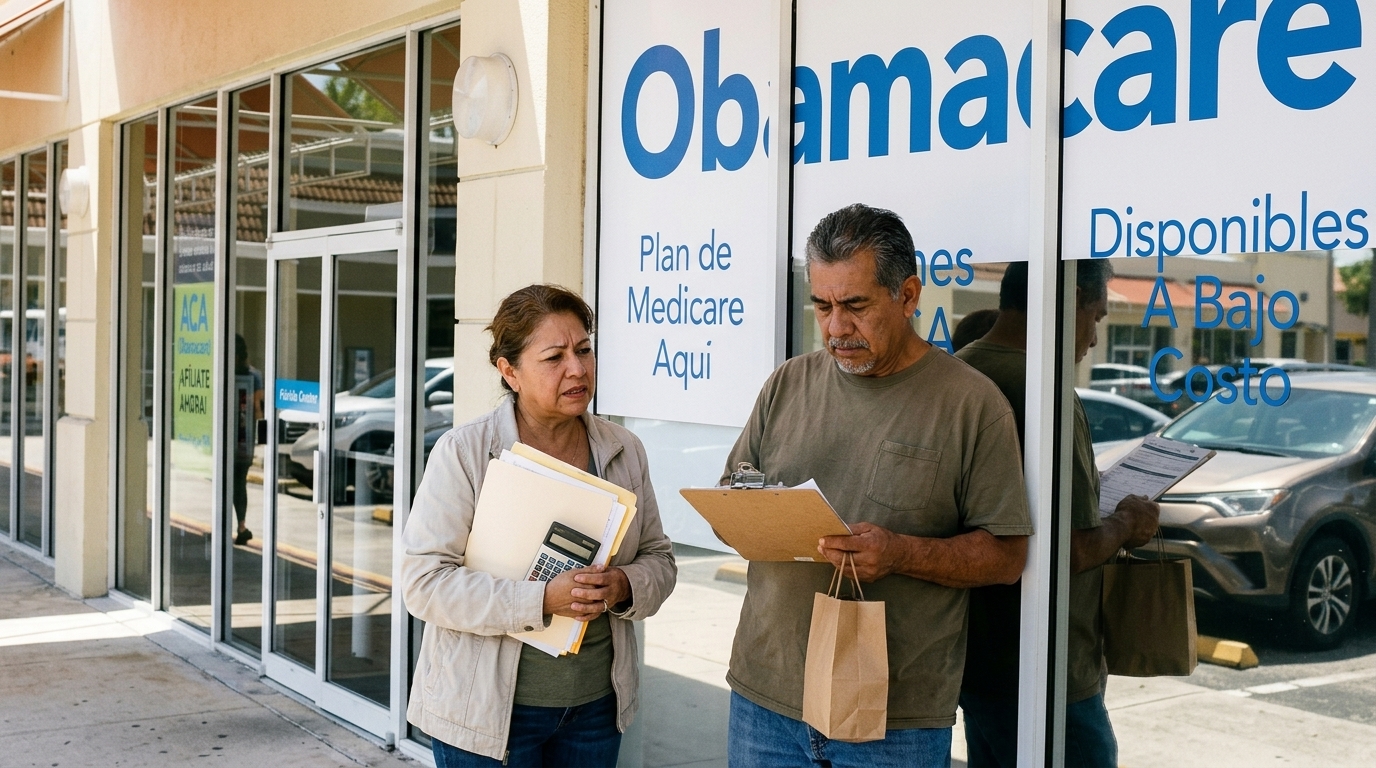

The American healthcare landscape is undergoing a sharp and painful recalibration. According to recent data, more than 3 million Americans have dropped their Affordable Care Act (ACA) coverage, commonly known as Obamacare, over the past year. This development is not a market fluke but the direct consequence of a deliberate political decision by Congressional Republicans to allow enhanced federal subsidies, established during the pandemic, to expire.

The End of the 'Golden Era' of Subsidies

For nearly five years, American citizens experienced an unprecedented level of access to affordable health coverage. Subsidies introduced via the 2021 American Rescue Plan and later extended by the Inflation Reduction Act (IRA) had brought premiums down to near-zero for millions of households. However, the refusal of the Republican majority to renew these tax credits has created what analysts term a 'subsidy cliff.'

The sudden price hike has forced many, particularly the working middle class, to re-evaluate their financial priorities. When a monthly premium jumps from $50 to $400, health insurance transforms from a basic necessity into a luxury that many can no longer afford. The Kaiser Family Foundation (KFF) warns that this is only the beginning, projecting that total enrollment could plummet to 17.5 million by the end of 2026, down from a peak of 19.2 million.

Political Deadlock and Fiscal Ideology

The expiration of these subsidies serves as the centerpiece of a broader ideological battle. Republicans argue that these enhancements were temporary emergency measures that ballooned the national debt and contributed to inflationary pressures. Their rhetoric focuses on fiscal responsibility and the necessity of returning to a market driven by competition rather than government intervention.

"We cannot continue to subsidize private insurance with money borrowed from future generations," a prominent Republican staffer noted during the budget debates.

Conversely, Democrats and public health advocates are sounding the alarm. They contend that the fiscal savings are illusory and short-sighted. The cost of millions of uninsured citizens will eventually manifest in overcrowded emergency rooms and uncompensated care costs for hospitals, which inevitably trickles back to the taxpayer in more expensive, less efficient ways.

Economic and Social Repercussions

The decline in coverage has immediate implications for household financial stability. Without insurance, a sudden illness or accident can lead to total financial ruin. Furthermore, the exodus of healthier individuals from the marketplace—who are typically the first to drop coverage when prices rise—creates a phenomenon known as 'adverse selection.' This leaves the remaining pool older and sicker, driving premiums even higher for those who stay, creating a destructive feedback loop.

- Surge in medical debt among middle-income families.

- Decline in preventative screenings and early-stage diagnoses.

- Increased strain on public safety-net hospitals from uninsured patients.

- Market volatility for insurers facing a shrinking and riskier customer base.

As we approach the next election cycle, the future of the ACA is poised to dominate the political discourse once again. The loss of coverage for 3 million people is more than just a statistic; it is a significant shift in the social contract, reflecting the deep divisions in how America views health as either a right or a commodity.